Real estate investment and advisory firm JLL has released its Q1 2016 Jeddah Real Estate Market Overview report today assessing the latest trends in the office, residential, retail and hotel sectors. In Q1 2016, it was noted that Jeddah witnessed a general slowdown across its real estate sectors due to demand-supply mismatch and the country’s overall macroeconomic scenario.

“The existing demand-supply mismatch is expected to widen as more retail and office supply is expected to enter the market with the easing of backlog projects,” observes Jamil Ghaznawi, national director and country head of JLL KSA.

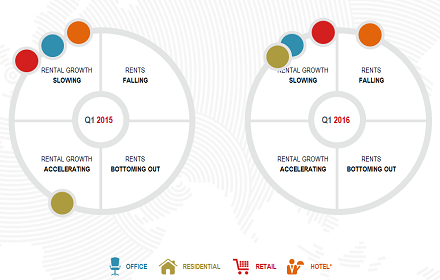

“In the residential segment, sales prices continued to decrease marginally, while rents started slowing down in Q1 2016 after continuous growth in 2015. It is also interesting to see that higher quality residential developments are being launched in response to buyer demand for additional amenities. On the other hand, the office market witnessed a further slowdown in the growth of lease rates, which is expected to continue due to demand constraints throughout 2016. Historically, the government and public sector have led demand for office space in Jeddah, but going forward we expect a shift in demand towards private firms as there is hardly any new project announcements,” he adds.

“Meanwhile, in the retail market lease rates have showed signs of stabilisation in Q1 as vacancies are absorbed. With more projects materialising over 2016/17, lease rates are expected to remain stable or decrease marginally. But with a year-on-year reduction of 9% in the value of retail sales, it could affect retail footfall which in turn will impact demand for retail space,” Ghaznawi continues.

The hotel market is impacted by the general economic slowdown as a result of lower oil revenues affecting various demand drivers. With declining visitors, the hotel sector has begun to show signs of weakening across Jeddah. Interestingly, new supply is expected to be added as a number of hotels are expected to be completed later in 2016, and it remains to be seen how they will perform in this economic scenario.

Retail sector summary highlights

The first quarter of 2016 saw two completions – Al Khayyat 3 and Yasmin Mall. These added just over 70,000 sqm of GLA to the market. The total supply of retail space currently stands at approximately 1.2 million sqm of GLA. While year-on-year lease rates have increased for both regional and super-regional centres, changes in quarter-on-quarter lease rates suggest that they have peaked as super-regional rates remain stable and regional centres decreased marginally by 1% as of Q1 2016.

Year-on-year vacancies have increased from 7-to-10% as vacancies increased in dated shopping centres, while they reorganise tenants and upgrade their facilities. Quarter-on-quarter vacancies have decreased marginally from 11-to-10% in as some refurbishments, such as in Mall of Arabia, are completed.

Higher materialisation is expected over the next two years after 2015 saw a slowdown in the number of projects entering the market. A further 56,000 sqm of GLA is expected to be delivered in 2016, while 2017-18 is expected to add over 900,000 sqm of retail space to the market in Jeddah. However, some delays and cancellations are expected.

Following the opening of Yasmin Mall, as part of Arabian Centres’ expansion plans across KSA, further three centres are expected to be delivered in Jeddah by 2018. These include Al Qalam Mall in King Abdulaziz University, Jawharat Jeddah in Al Basateen District and Prince Sultan Oasis which is a part of Prince Sultan Cultural Centre. For the first time in 10 years, point of sale transactions reduced 9% year-on-year. This is due to the recent cut in energy subsidies, which softened purchasing power in Saudi Arabia.

CEO’s Agenda: Unlocking the Treasure Chest of Retail Opportunities

Finding the treasure chest of opportunities needs years of journeying through the

January 19, 2024 | By RetailME Bureau

Culinary playbook: On a gastronomic adventure

How is the food service industry in the Kingdom of Saudi Arabia

January 18, 2024 | By RetailME Bureau

Launched in 2019 by Laura Manning, UAE-based homegrown brand BRW Society completes

Dr. Dhananjay Datar Chairman & Managing Director ADIL Trading Co. LLC holds

In 1995 regional retail conglomerate Majid Al Futtaim introduced Carrefour to the

Tata Soulfull, a leading name in the ‘good-for-you’ snacks and breakfast cereals

Majid Al Futtaim – Retail, which holds the exclusive franchise to operate

In an exclusive interview Krishna Dhanak, Managing Director, Alpen Capital shared insights

As digital transformation across the retail industry continues to accelerate, the expectations

Saudi Arabia-based grocery retail chain Al Raya Supermarket serves over 100,000 customers

BinDawood Holding has a rich Saudi heritage, spanning over 50 years, 38

Majid Al Futtaim Retail, which owns the exclusive rights to operate Carrefour

BinDawood Holding Company has earned an Honorary Shield, a distinguished recognition by

Dalma Mall is once again set to offer an unforgettable experience to

Arabian Center, launched its eagerly awaited Mall Gift Card, coinciding with the

Deerfields Mall welcomes an enticing lineup of new brands, each adding its

A key community-centered destination in Dubai, Times Square Center is actively championing

Shopping centres are the modern-day agoras, buzzing hubs where commerce meets community.

Attracting over 4 million in footfall, 2023 was a remarkable year for

Three of Majid Al Futtaim’s shopping malls in the region have been

A modern mixed-use development One Za’abeel, wholly owned by the Investment Corporation

Globally, retailers are becoming serious about their commitments towards creating business models

Cenomi Centers, one of the largest developers of shopping malls and complexes

Dubai Mall recently celebrated the grand unveiling of Chinatown, seamlessly integrating cultural

Curating and giving homegrown businesses a platform for growth has always been